A looming threat as year end approaches?

|

Bond markets often see lower liquidity towards year end, as the sell side prepares to slim balance sheets and the buy side closes books. However, wIth the current slew of negative factors, markets may experience more than just a seasonal liquidity slump. We’ve seen a steep rise in Covid-19 cases across Europe, with further lockdowns likely. The scale of the economic fallout from the pandemic is also starting to show, with rising unemployment, bankruptcies and lower than expected GDP growth. At the same time, we have uncertainty around the US election and a growing risk of a "hard" Brexit. March 2020 saw a major liquidity shock in € IG corporate bonds. This year end, we can hope for better, but should perhaps expect the worst. Is your € IG allocation ready for a re-run of March? |

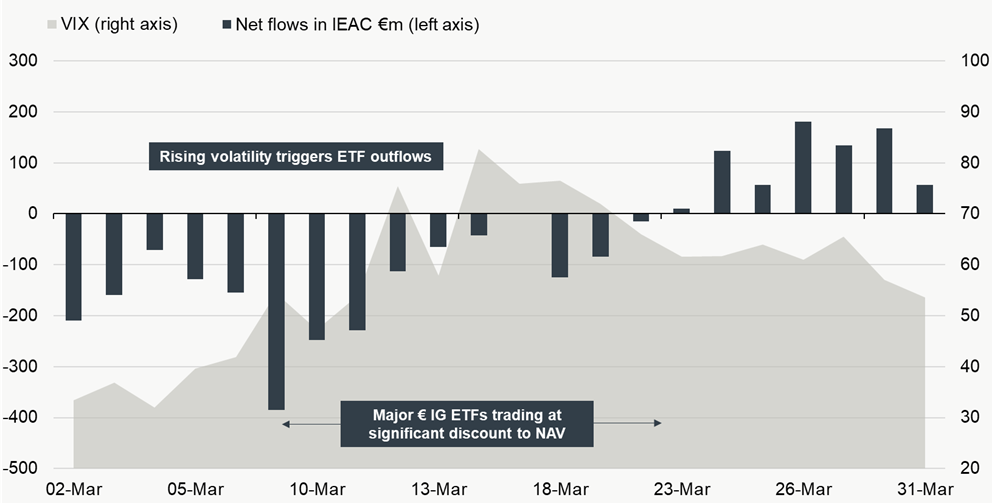

Lessons from March #1: large outflows and high discounts in € IG bond ETFs

In March, rising volatility triggered outflows across € IG corporate bond ETFs. Chart 1 shows the outflows in the largest of these, the iShares Core € Corp Bond UCITS ETF (“IEAC”), as market volatility rose. In this stressed market, many bond ETFs, including IEAC, traded at discounts of over 6% to their Net Asset Value as dealers had to price underlying bonds that weren’t trading.

CHART 1: March 2020, flows in major € IG bond ETF and market volatility

Data: ETFbook, Bloomberg, 15 October 2020. Past performance is not a reliable indicator of future results.

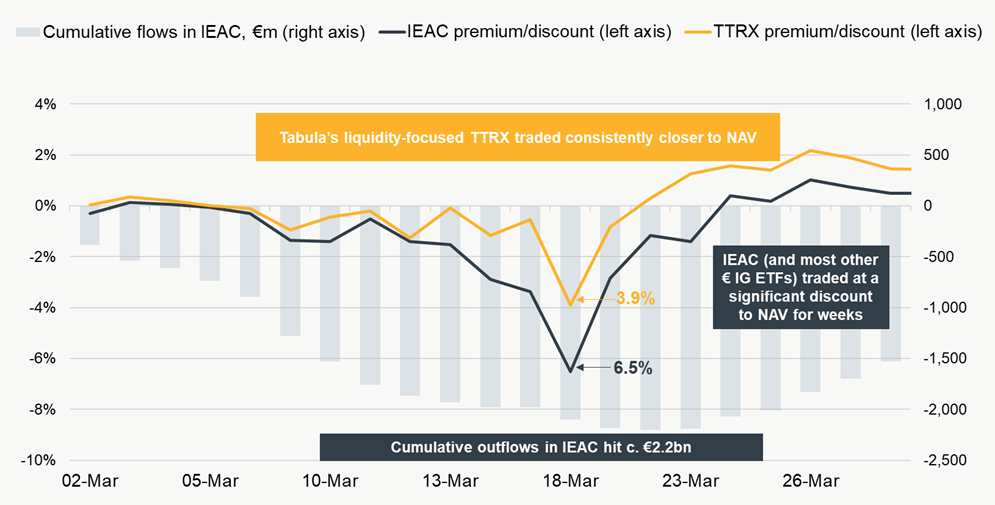

Lessons from March #2: Tabula’s liquidity-focused ETF was more resilient

Chart 2 compares the discount to NAV during March 2020 in iShares IEAC and Tabula iTraxx IG Bond UCITS ETF (“TTRX”), which provides European IG bond exposure with strict liquidity screening. As the chart shows, TTRX traded at a consistently smaller discount to NAV throughout March, with a discount of only 3.9% on 18 March versus over 6% in IEAC and several other large € IG ETFs.

CHART 2: discount to NAV in Tabula TTRX and iShares IEAC

Data: Bloomberg and ETFBook.com, 15 October 2020. Premium/discount is the % difference between exchange traded price and Net Asset Value (NAV). Past performance is not a reliable indicator of future results.

|

Why TTRX? Re-engineered € IG exposure Provides diversified investment grade bond exposure closely matching iTraxx Europe, the market standard for European credit trading Strict liquidity screening Targets large European issuers (up to 125, as per iTraxx Europe) and the largest, most liquid bonds with minimum outstanding of €500m European issuers only Reflects the European corporate credit environment and avoids the extra complexity of US issuer risk (some € IG ETFs have around 20% US issuer exposure) “Crisis-ready” Traded at a smaller discount than broad € IG ETFs during March 2020 and has overlap of ~80% with the ECB’s QE programme for corporate bonds |